-

A New Oil Crisis Stress-Tests the Global Energy Transition

April 22, 2026 By Jewellord Nem Singh

The US–Israeli war launched against Iran in 2026 may be remembered as the moment fossil-fuel dependence became more than a mere abstraction for the Global South. Brent crude quickly surged past $100 a barrel. Iran militarized the Strait of Hormuz (through which 20 million barrels a day, or a fifth of global oil consumption, normally flow) and retaliated against regional energy infrastructure. Qatar declared force majeure on its liquefied natural gas exports after Iranian drone attacks. Saudi Aramco’s Ras Tanura refinery shut down.

Fatih Birol, the head of the International Energy Agency, has labeled the conflict as the “greatest global energy security challenge in history.” The IMF’s Chief Economist Pierre-Olivier Gourinchas has warned that continued escalation could “cause an energy crisis on an unprecedented scale.”

Now the IMF has put numbers on the damage. The Fund’s April 2026 World Economic Outlook cut its 2026 global growth forecast to 3.1% and raised projected inflation to 4.4% under the assumption of a short-lived conflict. An adverse scenario that sees oil averaging $100 a barrel and Asian and European gas prices up 160%—pulls global growth down to 2.5% and inflation to 5.4%.

Many factors have come into confluence to create this crisis. The Trump administration’s decision to place American strategic interests above the global energy order is exacerbating an already-brittle and slow post-pandemic recovery—from which developing countries with thin welfare systems were already suffering. The risks to global poverty and growth achievements are clear.

Yet the new energy shock is exposing once again which developing economies in Asia, the Global South and elsewhere have the political capacity to cushion their markets from an external shock — and which do not. Many developing countries have quietly built an institutional capacity to withstand these disruptions, but the aggregate numbers reveal an asymmetry of state capacity: those countries least able to absorb the shock are the same countries most exposed to the crisis. What is unfolding now is not just another price spike; it is a structural test of the system.

Asia’s Philippines Stress Test

Emerging Asia is the epicenter of this new crisis. Regional growth is now expected to fall from 5.5% in 2025 to 4.9 in 2026 and 4.8 in 2027. Asian LNG prices have surged to 20.8 dollars per MMBtu, up 80.6% since August 2025. Nearly all regional governments source more than three-quarters of their LNG from suppliers who use the Strait of Hormuz. At the peak of the March shutdown, 8.5 million barrels of crude per day were curtailed.

No country illustrates the vulnerability more starkly than the Philippines. It imports between 95-98% of its oil from the Persian Gulf. Fossil-fuel imports already cost the economy the equivalent of 6.1% of GDP in 2022 and make up 50.6 % of total primary energy supply — a share the IMF projects to rise to 61.1% by 2050 on current policies.

When the Strait of Hormuz closed, national oil stocks fell from 57 days to 45 within a month. Diesel hit 130 Philippine pesos per liter; gasoline surpassed 100 pesos. President Ferdinand Marcos Jr declared a state of national energy emergency in late March 2026. He was the first head of state in the world to do so.

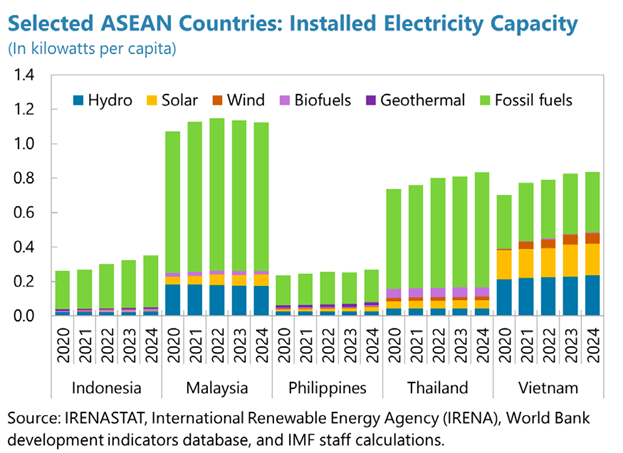

The IMF cut its 2026 growth forecast for the Philippines from 5.6 to 4.1 % — a 1.5% downgrade, one of the sharpest in Asia. Inflation is expected to breach the central bank’s target band at 4.3%, and the current-account deficit is projected to widen from –3.3% of GDP in 2025 to –4.4% in 2026. Yet these numbers underscore something even more striking: the Philippines already lags behind its ASEAN neighbors in terms of the broader renewable energy transition. (Figure 1.)

Figure 1: Comparison of Energy Matrix in Southeast Asia The government’s initial response was reactive: a three-month excise tax suspension on fuel, 20 billion Philippine pesos released from the Malampaya gas fund, and emergency diesel shipments from Malaysia. Transport strikes erupted across Manila as jeepney drivers—the backbone of its commuter system—saw their daily earnings collapse.

Opposition lawmakers want to repeal the Oil Deregulation Law of 1998, which stripped the state of pricing authority. Department of Energy Secretary Sharon Garin put the conundrum bluntly in a Senate hearing: “We are dependent on an industry [over which] the government doesn’t have any regulatory powers…” It is telling when a senior official publicly acknowledges the absence of a regulatory state.

Stop-gap measures do not address the larger structural question: why is the Philippines so energy-insecure despite its enormous solar, wind and geothermal potential, as well as the world’s second-largest nickel reserves? Why is a nation with a key role in green technology’s future still exporting raw ore and importing refined fuel?

The Global South’s Double Vulnerability

One paradox of the oil crisis is how developing nations have become exposed to fossil-fuel shocks amidst significant pressures from the global North to intensify and prioritize their own renewable energy and mineral-processing capacities.

Nowhere is the pattern clearer than in Southeast Asia. ASEAN’s oil and gas bill amounts to about 4% of regional GDP—nearly double Europe’s share—and the region practically lost access to energy resources when the Strait of Hormuz closed.

Some regional economies have better capabilities to ride out the crisis than others. Vietnam imports 85% of its oil (88% of that total from the Gulf) and holds just 30–45 days of reserves. Thailand is 69% import dependent. As net hydrocarbons producers, Indonesia and Malaysia do have meaningful buffers. In the case of the Philippines, which has the highest import dependence, highest Gulf concentration, and the largest IMF growth downgrade among ASEAN-5 economies, the implications are clear—even as the nation has attempted to pivot towards renewable energy with limited success.

Yet making a distinction between fossil-fuel and mineral security matters in this context. As the IEA has argued, oil price spikes hit every consumer immediately. Disruptions in critical-mineral supply affect only the production of new clean-energy infrastructure: electric vehicles, solar panels, batteries. Economies already powered by renewables are largely shielded from oil shocks, with China being the most notable example.

This dynamic reframes the politics of climate policy in the Global South. Every dollar invested in domestic renewable capacity and critical-mineral processing is simultaneously a climate investment and an energy-security investment. The latest oil crisis makes the case for the green transition more urgent, and not less. Governments must now be willing to achieve it.

Industrial policy as the missing link

My research through the ERC-funded GRIP-ARM project, which studies how resource-rich countries design industrial policy for critical minerals, demonstrates why taking action is so difficult. Energy transition is not accomplished through market signals alone. It requires deliberate state strategy.

Examine the countries which have moved up the value chain: China in rare earths and batteries, Indonesia in nickel processing, Chile in copper and lithium, Brazil in niobium and iron. These nations did so by combining long-term vision, concessional finance and strategic coordination between state and industry.

Where any of those elements was missing, countries remained trapped in the extraction model: digging, shipping, and struggling as commodity prices fluctuated. Success came when these nations positioned themselves in fiercely competitive globalized supply chains by identifying niche markets, developing technologies to solve specific problems, and supporting domestic capital even when it meant going against international trade rules.

Laying the cases of the Philippines and Indonesia side by side is revealing.

The Philippines is the world’s second-largest nickel producer, yet virtually none of its nickel is processed domestically into battery-grade material. In fact, over 90% of raw nickel ore goes to China. Its industry players also routinely complain that costly electricity makes processing unviable.

Recently, the nation’s Board of Investment effectively solicited foreign investors to take over the country’s flagship high-pressure acid leach (HPAL) plant in March 2026 after its operator Sumitomo announced a shutdown. Thus, Philippines’s delay in effective industrial policy left it compelled to auction off its only advanced processing facility to the highest bidder.

Indonesia chose a different path by weaponizing its resource endowment. Because that nation’s 2014 nickel export ban compelled foreign investors to process domestically, roughly 300 Chinese companies now operate nickel processing facilities in Sulawesi alone. Freeport-McMoRan invested US$3.7 billion in smelter capacity as a condition of retaining its mining concession.

The Indonesian model does have problems. Most nickel processing there remains powered by coal-fired plants, making its battery-grade nickel among the most carbon-intensive in the world. Major downstream buyers, including Ford, have yet pay a premium for cleaner alternatives, providing an uncomfortable reminder that industrial upgrades outside a push to energy transition simply displace environmental costs, rather than resolving them.

Industrial Policy: Progress Meets Challenges

Mining may have fallen behind in the Philippines, but the opposite has happened on the renewables front. Public support for clean energy is often high, despite a poor knowledge on the mineral-intensive nature of the undertaking. Renewable energy private investment grew 225% from 2021 to 2022, then reaching PHP 987 billion (or 231% growth) in 2023 thanks to wind farm investments. Total investments from solar, wind and hydropower in 2024 reached PHP 1.38 trillion.

One policy change has been central. A law intended to circumvent constitutional limits on foreign ownership was passed in 2022 to allow 100% foreign ownership of renewable energy projects. Subsequent efforts have developed essential new energy infrastructure.

Yet the institutional architecture of industrial policy remains a weak link, with coordination among lead agencies existing largely on paper. Meeting the Philippine Energy Plan’s own PHP 10.67 trillion RE investment target by 2050—about 40% of 2024 GDP—will require the kind of state capacity the country has not yet built.

Crucially, making effective use of strategic industrial policy in a country that embraced neoliberalism since the fall of the Marcos Sr. dictatorship in 1986 can only happen if citizens accept that not only the private sectors, but also the government, can deliver public goods.

The question of public investment comes to the front of such discussions. Both the mining and energy sectors are often oligopolistic, with large scale investments that take place over several years and attract little interest among smaller private actors. East Asian states have demonstrated that both the public and private entities must assume risks in the name of structural and industrial transformation—and then reap the shared rewards of shared economic growth.

Turning crisis into strategy

While such undertakings are rarely possible in peacetime, the new oil crisis could change this calculus. In the Philippines, Energy Secretary Sharon Garin, with the backing of President Marcos, has begun framing the expansion of electric vehicles and renewables as the long-term answer to the nation’s oil dependence, explicitly citing China’s success in insulating itself from oil shocks.

Yet while the fiscal pain of importing $100-a-barrel crude is a powerful incentive, the window for change is narrow. Solving only immediate needs will squander an opportunity.

First, oil-dependent developing countries must fast-track renewable deployment as a near-term energy security measure. Solar and wind bring no fuel costs. Once installed, they are immune to the Strait of Hormuz.

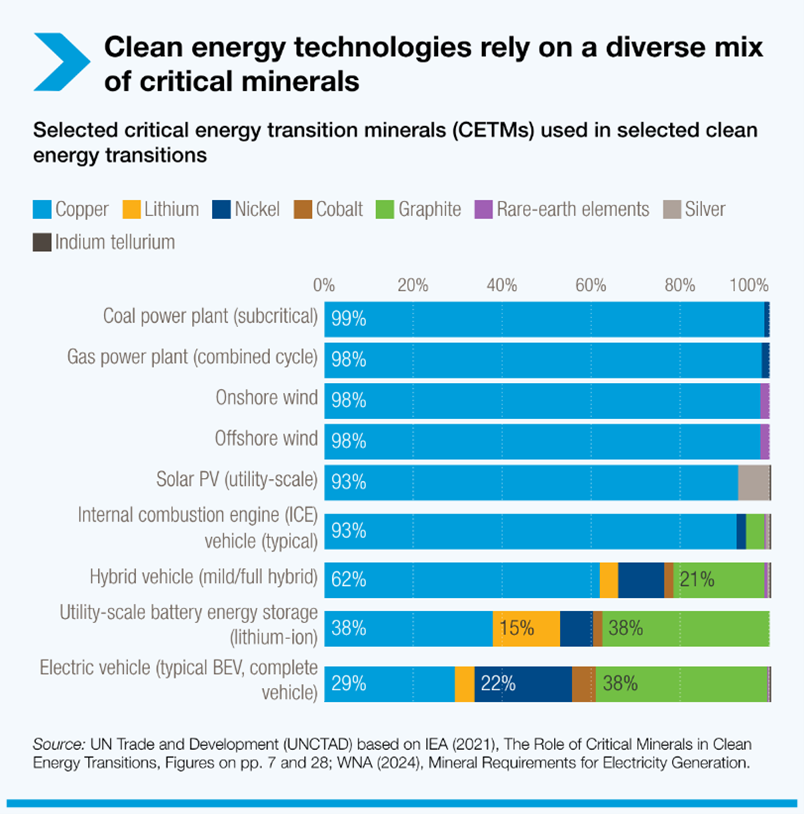

Mineral-rich developing countries also must treat their critical-mineral endowments as strategic assets rather than export commodities. Investments in domestic processing and demanding technology transfer from foreign investors must accompany greater state capacity to negotiate better terms. UNCTAD’s March 2026 report puts it directly: market forces alone will not deliver inclusive outcomes. The unprecedented demand from clean energy industrial players is precisely the leverage needed to push for upgrades in mineral processing, procuring the engineering know-how for new extraction technologies, and even a move into the components of renewable-energy technologies themselves.

Figure 2: Source Minerals for Clean Energy Transition Finally, the international community — and the United States in particular — must recognize the cascading consequences of the war for energy security and transition. While the US Inflation Reduction Act and the EU Critical Raw Materials Act were designed to build resilient supply chains, the foundations of these chains are located in countries now destabilized by oil price shocks. You cannot build a green supply chain on the backs of economies in energy crisis.

The oil crisis is not just about oil. It is a stress test for the global energy transition. Most of the developing world is failing that exam. Will their governments use this costly shock to build capability? Or will they choose to simply survive it—and wait for the next one.

Jewellord (Jojo) Nem Singh is Principal Research Fellow at the University of Sussex and Principal Investigator of GRIP-ARM (Green Industrial Policy in the Age of Rare Metals), funded by the European Research Council (Grant Agreement No 950056).

Sources: Al Jazeera; Business World; Context; Daily Tribune; The Deep Dive; GRIP-ARM; IEA; IMF; Middle East Eye; Office of the President of the Philippines; UNCTAD

Photo Credits: Licensed by Adobe Stock.

A Publication of the Stimson Center.

A Publication of the Stimson Center.